Our greatest responsibility is to be good ancestors.

—Jonas Salk

2008 is an election year, and it also triggers a very significant change in our demographics: the first of 77 million retiring Baby Boomers becomes eligible for Social Security benefits, which will create one of the greatest economic challenges of the 21st century.1

Baby Boomer Burden

Almost 10,000 new beneficiaries a day, 365 days a year, for the next 20 years, will begin drawing benefits. One of the greatest threats to the fiscal health of the United States is the runaway growth of the nation’s major retirement and health care entitlement programs.

Social Security, Medicare and Medicaid presently consume over 42% of the federal budget. Social Security deepened its financial abyss $200 billion deeper over the past year; Medicare’s abyss deepened by $2.8 trillion!2

Social Security, Medicare and Medicaid presently consume over 42% of the federal budget. Social Security deepened its financial abyss $200 billion deeper over the past year; Medicare’s abyss deepened by $2.8 trillion!2

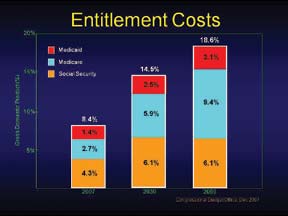

The Congressional Budget Office projects that federal spending on Social Security, Medicare and Medicaid will leap from 8.4% of GDP today to 18.6% by 2050 (see chart left). And these projections ignore the lingering impact of the 20 million illegal aliens also lining up for these benefits.

There are three prevalent myths about this debacle:

1. We can make up the deficits with economic growth.

2. We can avoid catastrophe by eliminating government waste.

3. We can raise taxes to solve the problem.

All three are fallacious and prey on the naive. If taxes are increased to cover these costs, the levels required would have an extremely negative impact on employment, wage growth, and our ability to compete internationally.

On the other hand, borrowing to pay for these programs will lead to such high deficits that the resulting debt would be unsustainable.

The Urgent Preempts the Important

Our strategic perspective is now also being eclipsed by our tactical predicament. What many believe is the greatest financial crisis in U.S. history is now making its appearance: the stock market is plunging from its previous highs; the real estate meltdown is accelerating; bank runs are proliferating; and, bankruptcies, foreclosures, and job layoffs are skyrocketing.

A Picture is Worth 1024 Words

This is not just alarmist propaganda. Check out any of the figures yourself (see charts): General Motors, once one of our proudest exemplars of sound management, is now struggling for its survival.

This is not just alarmist propaganda. Check out any of the figures yourself (see charts): General Motors, once one of our proudest exemplars of sound management, is now struggling for its survival.

The FDIC is reported as having a secret list of 90 troubled banks that are in danger of failure3 (see chart left).

Remember, the FDIC is only a psychological safety net: it only has enough funding for a fraction of what it may be facing. And the real estate mortgage picture continues its dismal plunge (see chart right):

Retail sales, manufacturing, and the travel and hospitality industries are plunging. (Starbucks is closing 600 stores.) Airlines are increasingly characterized by cancellations, confusion, and abusive management practices. [A personal example: it took us 36 hours to accomplish a four-hour flight this past weekend. Unfortunately, that is increasingly becoming a common experience.]

As oil—and other commodities—continues into the stratosphere, personal disposable income, consumer confidence, and spending continue to decline at the fastest rate since the Great Depression. (In contrast to the 1930s, however, our current culture is now no longer benefited by the work ethics and self-reliance that characterized those earlier challenging generations.)

So it is a time for each of us to position ourselves, as much as our individual means may allow, for the approaching storm.

So it is a time for each of us to position ourselves, as much as our individual means may allow, for the approaching storm.

It is a time to preserve our assets—especially our liquidity—and to prioritize our commitments in accordance with whatever our King has called us to. It certainly should be one of the most fruitful times for the Body of Christ for those who are called—and prepared—for His purposes. People who have previously been complacent and apathetic will be desperately looking for answers. Are you prepared to provide them?

It is a time to preserve our assets—especially our liquidity—and to prioritize our commitments in accordance with whatever our King has called us to. It certainly should be one of the most fruitful times for the Body of Christ for those who are called—and prepared—for His purposes. People who have previously been complacent and apathetic will be desperately looking for answers. Are you prepared to provide them?

Notes:

- These figures refer to the change from 2006 to 2007 in the unfunded obligations in Social Security and Medicare on an infinite-horizon basis.

- ABC News, 7/15/2008.